Retirement Withdrawal Rate Action Plan

Build a flexible retirement income system that adapts to any market environment

Based on: The Retirement Safety Margin Is Shrinking by Erin Talks Money

Build a flexible retirement income system that adapts to any market environment

Based on: The Retirement Safety Margin Is Shrinking by Erin Talks Money

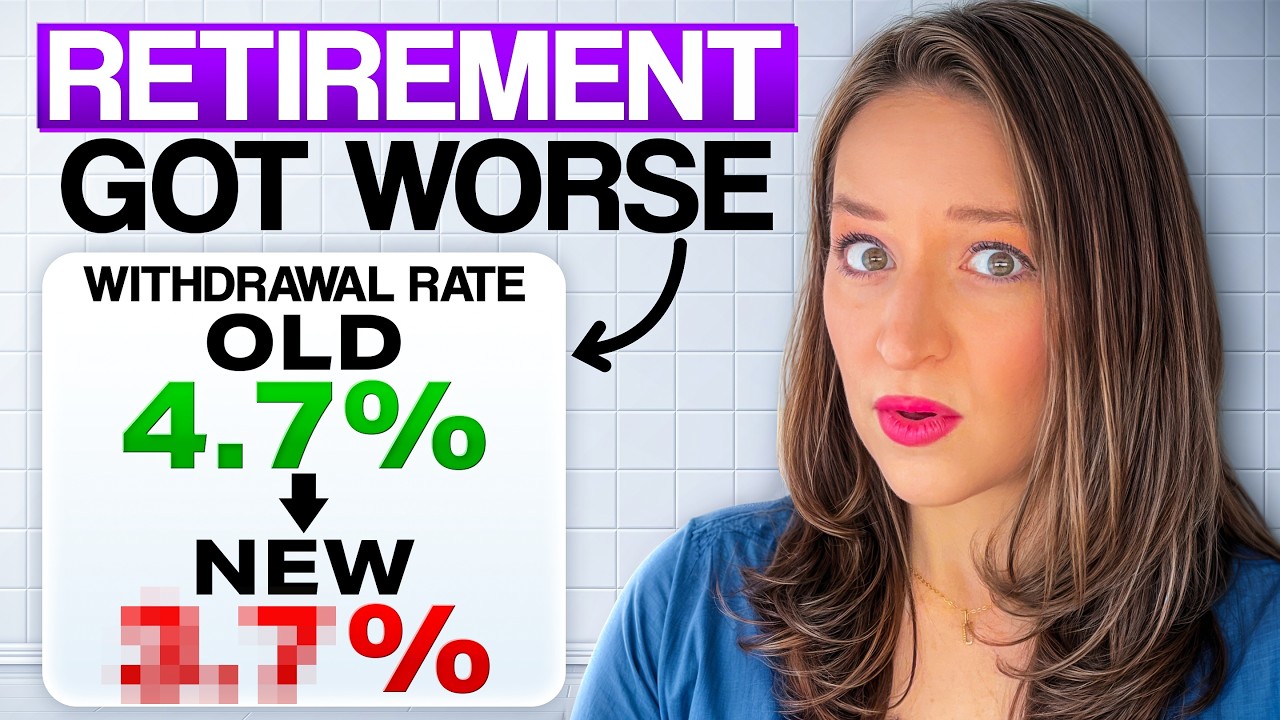

What if the number you've been building your entire retirement around is wrong — not because you did anything wrong, but because that number was never meant to be fixed in the first place? Most people approaching retirement latch onto the 4% rule like it's gospel, set their withdrawal rate on day one, and never look back. But here's what the research actually says: that approach can quietly hollow out a retirement plan, especially if you retire into a tough market environment. The stakes are real. Retire into high stock valuations and low bond yields — think 2000 or 2021 — and a rigid withdrawal strategy can leave you selling assets at exactly the wrong time, locking in losses, and watching your portfolio erode faster than you ever imagined. The sequence of those early returns matters more than almost anything else, and most retirement guides don't tell you that clearly enough.

Imagine instead walking into retirement with a living, breathing income system — one that tells you exactly what withdrawal rate makes sense given today's market conditions, how to stress-test your plan in years one through ten, when to pause inflation raises, when to trim discretionary spending, and when you've actually earned the right to spend more. That's the difference between a plan that looks good on paper and one that holds up in real life. Picture yourself in year 25 of retirement, more confident about your spending than you were in year three — gifting to family, taking that extra trip, because your system adapted and your portfolio survived.

Erin from Erin Talks Money has spent years translating complex retirement research — from Bill Bengen's original 4% rule study to Michael Kitces's CAPE ratio work, David Blanchett's valuation modeling, and Morningstar's annual State of Retirement Income report — into plain language that actually helps real people make better decisions. This checklist distills everything from that research-backed video into a clear, step-by-step action framework you can start using today.

This PDF checklist walks you through every phase of building a flexible retirement income system: assessing the market environment you're retiring into, choosing a prudent starting withdrawal rate, stress-testing your plan, knowing exactly which levers to pull when things get hard, and understanding when your plan has earned the right to relax. Stop searching for a single magic number. Start building the system that actually works.

Every checklist item comes with actionable notes to guide you — things like "Don't forget to do this before you start," "Avoid this common mistake," or "Set a reminder for 30 days out." Nothing vague, just clear next steps.

+ 20 more action items inside...

Instant PDF download. Start taking action today.

✓ Instant download · ✓ PDF format · ✓ No subscription